The Fed may have to balance balance sheet up again

The Treasury market is facing a patch of supply-related crosscurrents that may complicate the path for yields as they move higher.

Is it possible to wear an N 95 or KN 95? In 2022, Moderna Chair Says that No Covid Pandemic May Shift to Endemic in 2022.

None of the scientists have discovered a gene that increases the risk of dying from Covid.

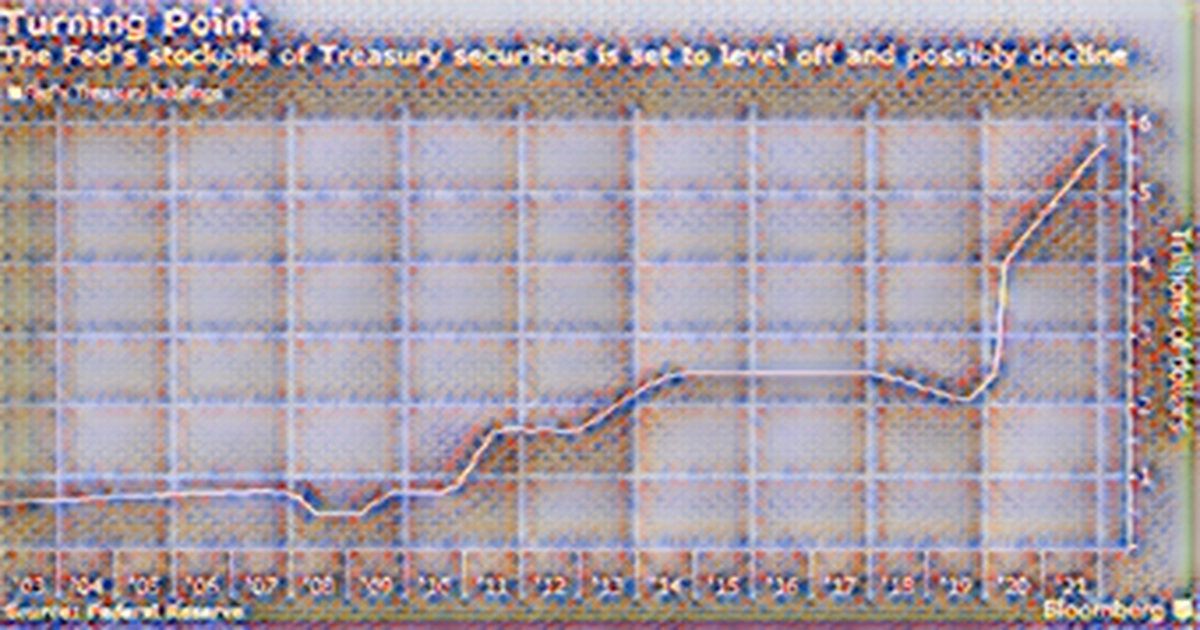

That course will get backing from the Federal Reserve's recent reduction in U.S. bond purchases, which will buy just $40 billion of Treasuries over the next month, half of the amount they once gobbled up. They won't happen for the first time since the most recent program of quantitative easing began in March 2020. When dealers announce its quarterly plans for sales, they will be busy estimating how much the Treasury department will trim the size of its auctions.

Yields on US debt maturing in the coming decade have gone up in the past two weeks back to levels seen before the epidemic roiled global markets in early 2020, with the rate on the benchmark 10 year note climbing more than 25 basis points this year. The Fed is expecting to raise overnight interest rates at least three times this year, if not four, and that it will eventually stop replacing the Treasuries it holds when they mature. The decision may not come before March when the programing adds new assets to the balance sheet is due to end.

William O Donnell, strategist at Citi, said that if the Fed dials back its bond buying it's pace is akin to loosening the nuts on the training wheels and the bike will be a little wobbly for the market to ride. The question is how much of the Fed buying less Treasuries is already priced in by the market given the rise in yields we have seen so far this year. The Fed's latest tapered purchase schedule includes 10 operations from Jan. 18 to Feb. 10. The previous month's schedules have had 18 operations, typically one each trading day.

The purchases, which have added $3.12 trillion of Treasuries to the Fed's stockpile since March 2020, have left a huge footprint. The purchases continued as a way to further support the U.S. economy after the Fed's policy rate was cut to around zero as the onset of the pandemic led to wholesale dumping of financial assets.

Market-moving on several occasions has resulted in a number of market-moving decisions about how to allocate its purchases across the maturity spectrum, despite the fact that all of the purchases are done according to a pre-announced schedule. The Fed's decision to less buy Treasury dealers leaves them more at the mercy of investors.

On balance, we can expect more volatile coupon auctions, as there will be more supply for the market to buy, O Donnell said.

The yield was 1.78% at the end of Friday, marking its fourth straight week-on-week increase. The last year, the first annual decline since 2013 for the Treasuries, has lost 1.8%, on top of a 2.3% loss last year, which is the first annual decline since the Bloomberg Treasury Index.

Morgan Stanley analysts predict that the 10-year Treasury yield will rise to 2.2% in the second quarter and 2.3% by the end of the year. They predict that the Fed will raise rates by 25 basis points each quarter. Money-market traders, who had previously predicted the Fed to keep rates unchanged through the end of the year, now assign 100% odds to hikes beginning in March. Three rate increases this year are forecast by the Fed in December, but several this month have said a March hike is needed to combat the hottest inflation in a generation.

The Treasury Department, which reduced the size of coupon-bearing dsebt auctions in November for the first time in five years to bring them in line with lower-than anticipated government expenses, is expected to do so again in February, regardless of the Fed's plans. On Friday, a quarterly survey of primary dealers asked for their views on how a decision by the Fed to allow its holdings to run off could affect financing needs and issuance decisions. The prospect of the Fed allowing some of its Treasury holdings to mature probably won't forestall auction size cuts in February, but it makes subsequent reductions less likely, said Lou Crandall, chief economist at Wrightson ICAP LLC.

As we move through this year, we will in all likelihood not know the future but if things develop as expected, we ll be normalizing policy," said Jerome Powell, chairman of the Senate Banking Committee Tuesday. We are going to end our asset purchases in March, we will be raising rates over the course of the year and maybe later this year we will start to allow the balance sheet run off. The Fed's next two-day meeting will be held on January 26. While interest-rate strategists believe that a decision on balance sheet runoff will be made in June, messaging may start sooner.

Matthew Hornbach, global head of macro strategy at Morgan Stanley, said investors are debating what the Fed will tell us at the end of the month. Most investors looking at Treasuries will err on caution until after the January Fed meeting. The financial markets of the U.S. will not be closed on January 17 in observance of Martin Luther King Jr. Day.

No Fed officials have no scheduled appearances during their self-imposed quiet period through the Jan. 25 -- 26 Federal Open Market Committee meeting.

None A $13 billion Bet That Air Travel Will Soon Take Off is a $13 billion bet on it.

Big Banks Fight Back in Washington as Fintech Eats Into Profits, Big Banks Fight Back in Washington.

Stupide says that it's the economy, not Macron and France.

In 2022, none of the central banks, not Covid, will drive global Economies.